The most and least expensive cities for home insurance in Ontario have been revealed in a new report.

Along with groceries and gas, home insurance costs have increased.

Ontario home insurance premiums are up 6.2 per cent year-over-year in 2026, according to a report from Rates.ca, an insurance rate-comparison platform.

Rates.ca released its Home Insuramap data report today.

The report looks at how home insurance premiums have changed across Ontario in 2026, including which cities are seeing the highest and lowest premiums, where costs are rising or falling year-over-year, and how property risk varies by geography.

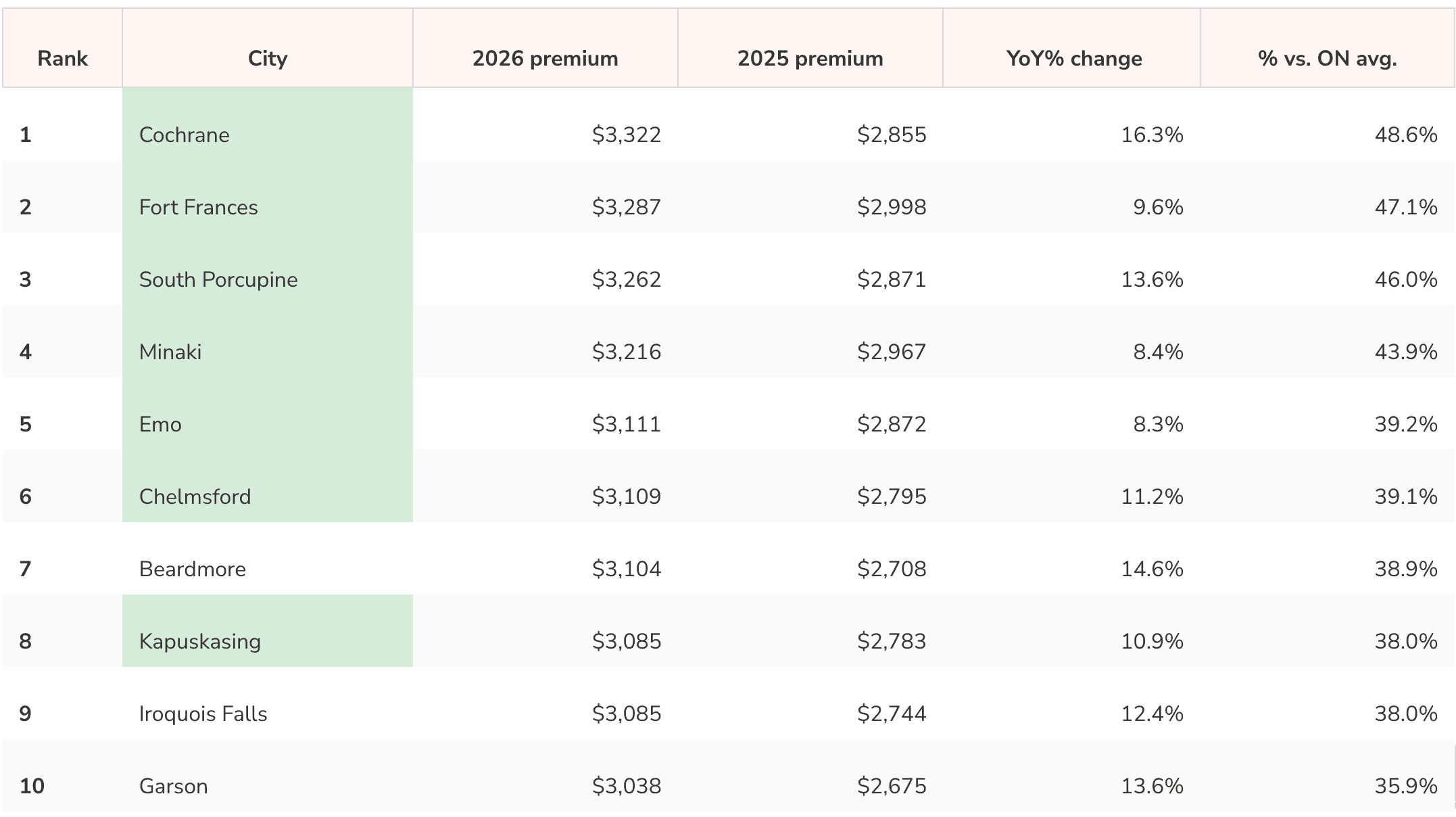

As in previous years, Northern Ontario cities topped the list with the highest home insurance rates, the report found.

Northern cities have historically had higher premiums than their southern counterparts. Many of these cities are in remote areas, which often means high rebuild costs and poor access to essential services, the report states.

Fewer contractors in those areas leads to higher demand for their labour, and therefore, higher costs. Building components also tend to be in short supply in those areas, necessitating additional transportation costs.

Here are the most expensive cities for home insurance in Ontario:

Chart: Rates.ca

Homes closer to emergency services will also have lower rates.

Insurance companies often factor in proximity to fire services and hydrants when pricing home insurance policies, said Steve Cohen, Rates.ca’s vice president of insurance and chief underwriting officer.

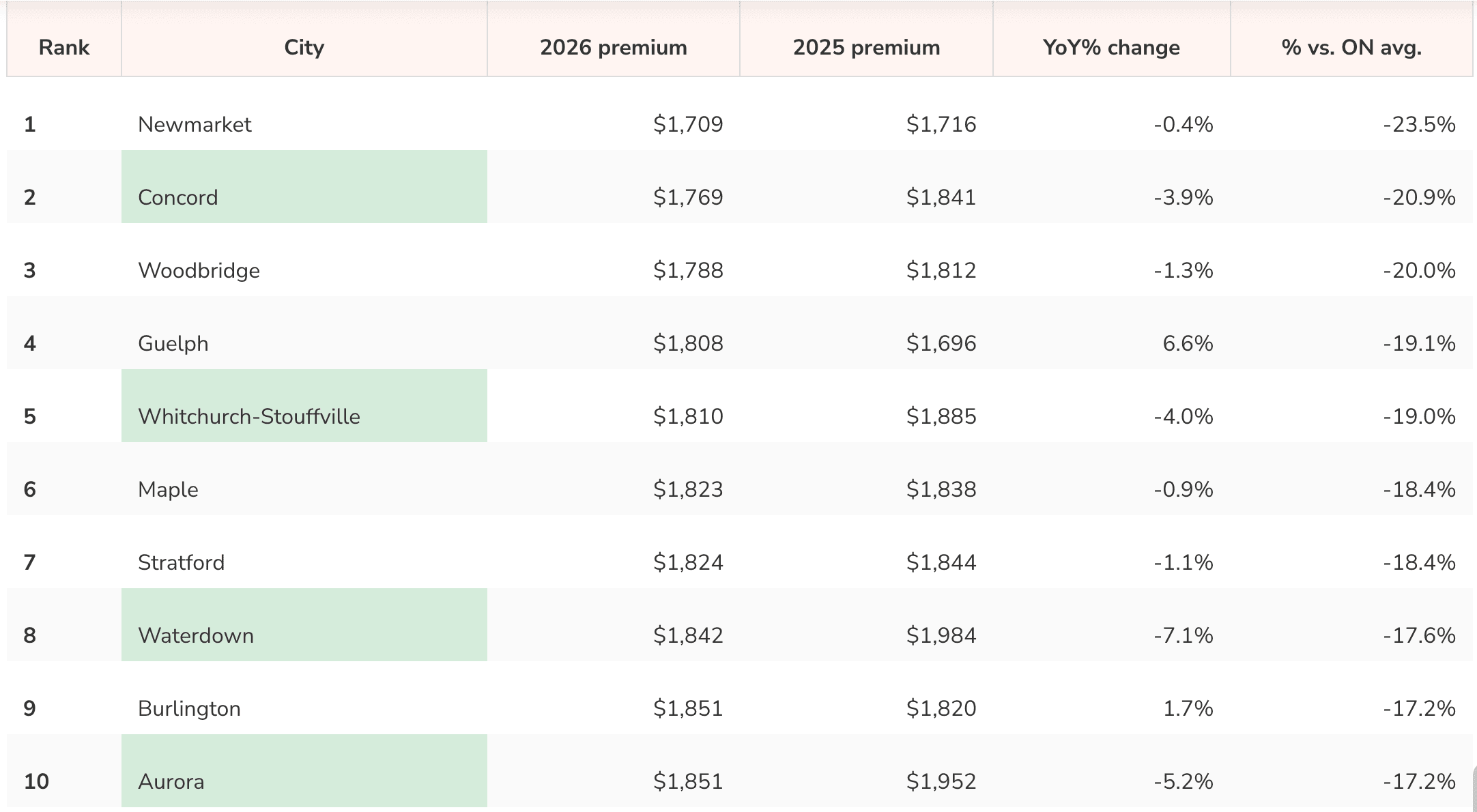

Southern Ontario cities dominate the least expensive list, with Newmarket having the lowest premium, at $1,709 per year, 23.5 per cent below the provincial average.

Here are the least expensive cities for home insurance in Ontario:

Chart: Rates.ca

Aurora, Whitchurch-Stouffville, and some areas in Burlington, Guelph, and Woodbridge have a low-risk profile that aligns with their least expensive premium ranking, the report states. But in other areas, home insurance pricing is nuanced and not always directly correlated to peril scores.

The Home Insuramap tracks five risks across Ontario neighbourhoods, including flood risks from external sources, such as heavy rainfall, snowmelt, or overflowing rivers; flood risks originating from backed up sewers, sump pumps and septic tanks; wind and hail damage; crime from thefts; and wildfire.

A high-risk profile reflects a score of high or extreme risk in three or more perils; and a low-risk profile reflects a score of low to medium risk in three or more perils.

More than half of Ontario—267 of 517 postal code areas—score high on crime risk.

In an insurance context, this refers to theft only and is weighted on the value of goods stolen.

A high crime rating should not be taken as an indicator of frequency or prevalence of break-ins or number of claims, the report states.

For example, a single claim with a high value of goods stolen could result in a high crime rating for a neighbourhood. It also excludes other kinds of crime, such as assault or drug trafficking. But an elevated risk profile for crime doesn’t translate into higher home insurance premiums.

In Brampton, for example, 90 per cent of neighbourhoods carry high crime risk, yet many of those areas still sit below the Ontario average premium of $2,235.

“Below-average home insurance premiums in Brampton aren’t necessarily a mystery or mis-pricing,” says Mayer. “They reflect newer housing stock, manageable claims history, and the simple fact that crime carries less weight in pricing than people think.”

For example, seven of the ten least expensive areas in Ontario—including parts of Mississauga, Richmond Hill, Ottawa, Burlington, and Markham—all have a high-risk profile for crime. Yet their premiums remain among the lowest in the province. It’s a signal that a high crime rating alone doesn’t drive insurance pricing.

“Crime is a real input into home insurance pricing, but it is a minor one compared to water, fire, wind, and rebuild costs,” said David Mayer, director of insurance at Rates.ca. “The crime penalty in home insurance is far smaller than most consumers expect.”

In southern Ontario, flood risks originating from backed-up systems such as sewers or sump pumps are an issue.

Areas with system backup risks sit in the Greater Toronto Hamilton Area—Toronto, North York, Etobicoke, Scarborough, plus Brampton, Mississauga and Hamilton.

This is because GTHA basements aren’t often bare concrete, they’re finished living spaces with expensive utilities.

“When your heating system gets wet, that gets very expensive,” said Dr. Jason Thistlethwaite, associate professor at the University of Waterloo’s School of Environment, Enterprise, and Development.

See the full report here.

Check the risk with your postal code here.

INsauga's Editorial Standards and PoliciesPollView All

WIN A $100 GIFT CARD

Subscribe to INsauga’s daily email newsletter for a chance to win a $100 Amazon gift card.