It Will Take Median-Income Earners 32 Years to Save Average House Downpayment

Published September 26, 2019 at 5:03 pm

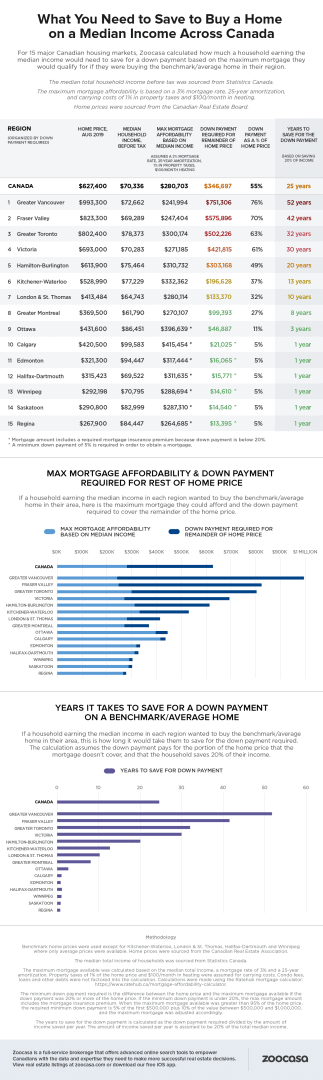

According to a new report from Zoocasa, it will take a median-income earner in Greater Toronto 32 years to save for a downpayment on an average house.

The report, released Thursday (Sept. 26), looked at 15 markets across the country to see how feasible would it be for a household on a median income to purchase real estate.

Eight of the markets in the study were found to be affordable and a median-income household would be able to save up the required down payment in less than a decade.

In the remaining seven, however, a median-income earner wouldn’t qualify for a mortgage large enough to fund their home purchase and would need to supplement it with a huge down payment.

In some of these markets, assuming 20 per cent of their income was being set aside, it would require a savings timeline that spans decades.

In the GTA, the median income is $78,373 and the average home price is $802,400. In order to afford a mortgage — a three per cent mortgage over 25 years, which includes $100 for heat and one per cent property taxes — on this home, one would need a 63 per cent downpayment, or $502,226.

Videos

At those rates, the median income earner in the GTA will have to put aside 20 per cent of their income for 32 years.

That might seem like a ridiculous timeline, but in Greater Vancouver, their timeline is 52 years.

The more affordable cities in Canada are Calgary, Edmonton, Halifax-Dartmouth, Winnipeg, Saskatoon and Regina, where a median income earner would have to save for a year.

It should be noted, that in these figures, condo fees, loans and other debts were not factored into the calculation.