As flooding risks increase, insurance rates spiked in some Ontario communities, a new report has found.

Rain is typical in the spring, but increasingly frequent heavy rainfalls have led to major flooding, states of emergency and preventive measures such as evacuations.

These storms are causing billions of dollars of damage annually, making flooding one of the country’s most destructive natural disaster, according to a 2024 report from the Insurance Bureau of Canada. Over a two-day period in the summer of 2024, flash floods resulted in $940 million in insured damage.

Home insurance rates have increased by 20 per cent since 2024 in some of Ontario’s most flood-prone housing markets, including some pockets of the Greater Toronto Area, according to a new report from Wahi, a Canadian real estate platform, and MyChoice, an insurance-rate aggregator.

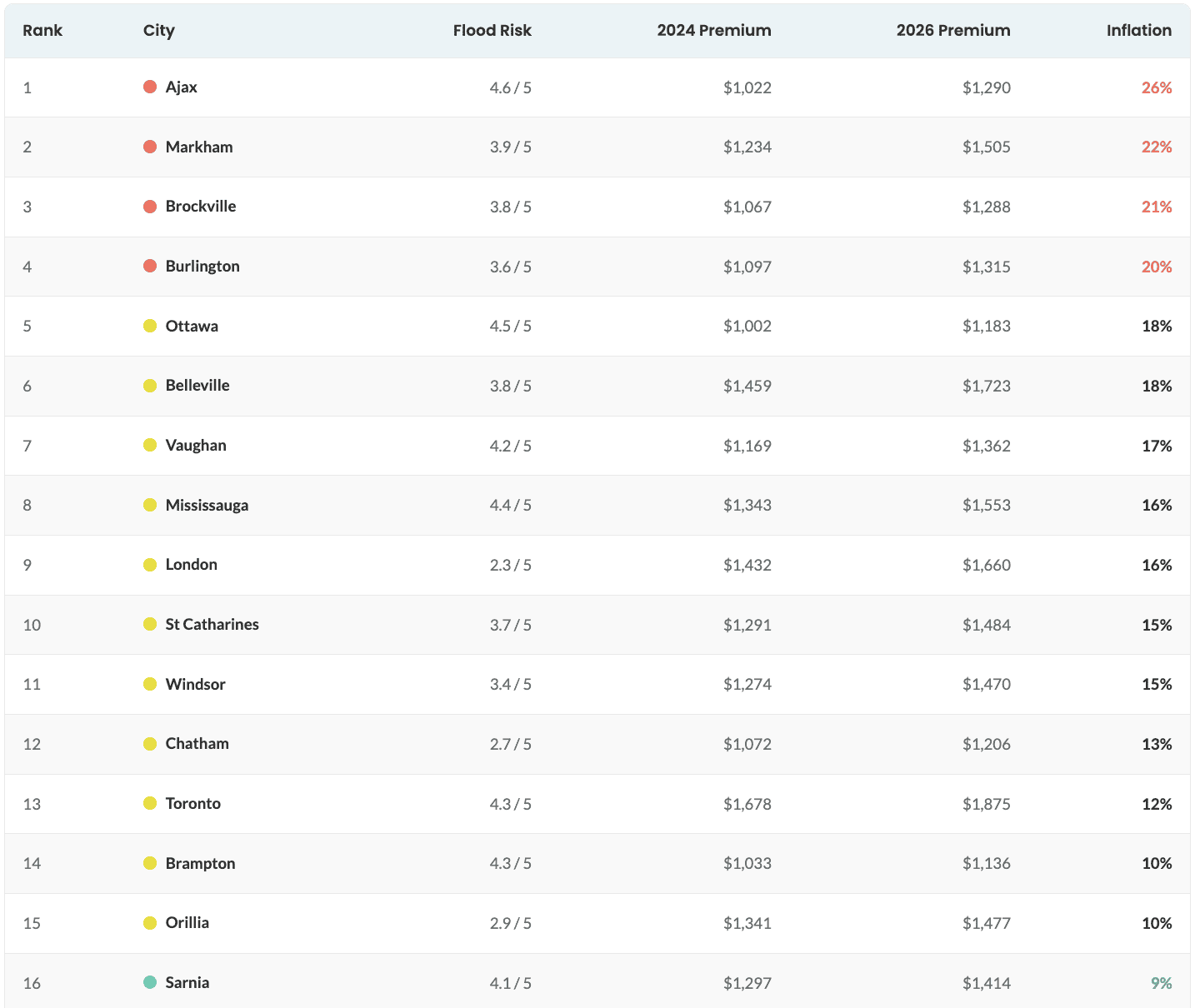

Of the 22 markets that had flood risk scores of at least three out of a possible five points, Ajax experienced the highest home insurance inflation, surging 26 per cent between 2024 and 2026. Ajax also had the highest flood risk score in the province (4.6), far above the provincial average (3.4).

In terms of home insurance inflation, Ajax was followed by another GTA market, Markham, where the average premium spiked by 22 per cent and the flood risk score was 3.9.

Brockville and Burlington were the only other cities with flood risk scores north of three and home insurance inflation of 20 per cent or more.

In Brockville, which had a flood risk score of 3.8, the average insurance premium has surged 21 per cent, while in Burlington, where the flood risk score was 3.6, premiums increased by 20 per cent.

Chart: MyChoice and Wahi

Annual home insurance costs were below $2,000 in the most flood-prone markets, with Toronto being the most expensive ($1,875) and Brampton the least expensive ($1,136).

“The average Ontario household pays less than $1,500 per year on home insurance,” Wahi economist Ryan McLaughlin said.

Looking at all 38 major cities, even greater insurance premium inflation was observed in Northern Ontario. This occurred despite generally lower flood risk scores. For example, premiums soared 31 per cent in Thunder Bay and 27 per cent in North Bay, though these markets had flood risk scores of 2.6 and 1.8, respectively, the report noted.

High insurance premiums in Northern Ontario may be related to higher labour and material costs in more remote regions, and the risks associated with wildfires.

See the full report from Wahi here.

Lead photo: Serge Lavoie

INsauga's Editorial Standards and PoliciesPollView All

WIN A $100 GIFT CARD

Subscribe to INsauga’s daily email newsletter for a chance to win a $100 Amazon gift card.